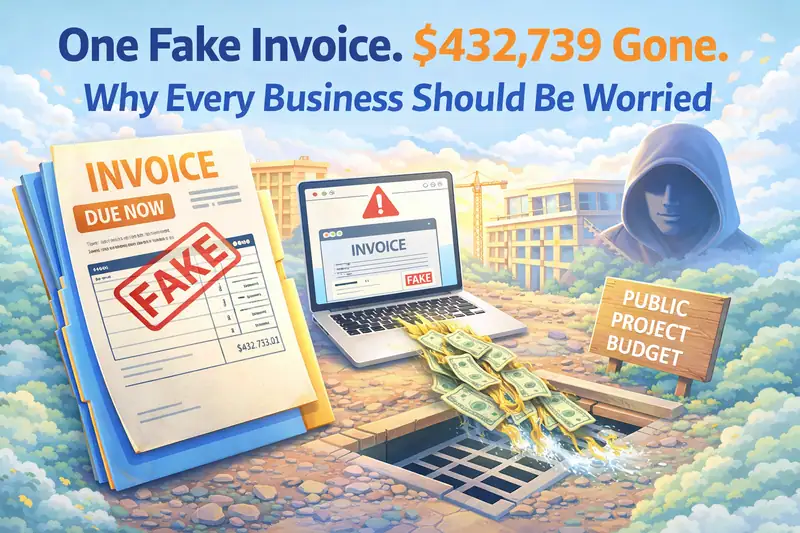

One Fake Invoice. $432,739 Gone. Why Every Business Should Be Worried

It did not start with ransomware.

Nobody kicked down the digital front door. Nobody lit up a screen with a skull, a countdown timer, and a demand for Bitcoin. Nobody needed a zero day, an elite exploit chain, or some ridiculous hacker film soundtrack.

Instead, someone sent what looked like an ordinary business message connected to a real construction project.

Then the money moved.

The City of Arab, Alabama says it lost $432,739.21 after an unknown individual posed as a legitimate officer of the contractor building its new Recreation Center and redirected a payment to an unauthorised entity. One fraudulent invoice. One redirected payment. Nearly half a million dollars gone. According to the city, the incident was a one time invoice fraud and payment redirection scheme. No citizen or employee data was breached. The wider systems remained secure. The damage came from trust being abused, not from a firewall being smashed open.

That should worry you.

Why?

Because too many businesses still imagine cyber risk as a bloke in a hoodie trying to brute force a password at three in the morning. That happens, of course. But this sort of fraud is often quieter, cleaner, and in some ways more dangerous. It slips past the mental picture people carry around in their heads. It does not look like “cyber”. It looks like accounts payable doing its job.

And that is exactly the problem.

The kind of attack that looks boring right up until it is not

Picture the scene.

A normal working day. Invoices moving. Projects underway. Suppliers chasing payment. Staff trying to keep things flowing. Someone in finance sees a message that appears to fit the pattern of the work already happening. The contractor is real. The project is real. The timing makes sense. The amount, while painful, may not even look unusual in the context of a major build.

So the payment gets processed.

Only later does someone realise the bank details changed when they should not have. Or the sender was not quite who they seemed. Or the thread was not genuine. Or the approval process was weaker than everyone assumed.

By that point, the money has legs.

That is what makes Business Email Compromise and invoice fraud so nasty. It does not need to break the locks if it can persuade you to open the door yourself. It does not need malware if a convincing lie will do the job more neatly. It does not need to “hack” the way most people think of hacking. It just needs somebody busy, somebody trusting, and a process with a soft underbelly.

That is not a technology problem alone. It is an operational risk. A finance risk. A governance risk. A training risk. A leadership risk.

So ask yourself this.

If one believable email landed in front of your team this afternoon, what would stop the payment leaving?

If your answer is “our people would spot it”, I would gently suggest that hope is not a control.

What actually happened in Arab

The city’s own statement is blunt enough.

It says officials discovered they had been the victim of a “sophisticated, socially engineered phishing scheme” tied to the construction of the new Recreation Center. An unknown individual or individuals allegedly posed as a legitimate officer of FITE Construction and caused a fraudulent payment of $432,739.21 to be issued to an unauthorised entity.

The city says it was a one time occurrence involving a fraudulent invoice and payment redirection scheme. It also says no personal, employee, or citizen data was accessed, and that the matter is under active investigation by local police, ALEA, the FBI, DHS, and the United States Secret Service.

Read that again.

This was not a technical smash and grab. This was a financial confidence trick delivered through business communications.

That matters because so many organisations still put cyber fraud into the wrong mental box. They shove it under “IT issue” and move on. Then finance owns payments, procurement owns suppliers, operations own projects, and leadership assumes somebody else has the ugly bits covered.

Meanwhile, the criminal just needs the gaps between those teams.

Why UK businesses should care about a city in Alabama

Because geography does not protect you.

Because sector does not protect you.

Because company size definitely does not protect you.

Small businesses in the UK are often even easier targets than municipalities. Why? Because they are busy, under resourced, and running on trust. One person may raise the purchase order, approve the invoice, and release the payment. A change of bank details may arrive by email and get accepted because the supplier relationship feels familiar. A “quick one before close of play” message lands at 4:47 p.m. on a Friday and somebody wants the backlog cleared.

That is the sweet spot for invoice fraud.

It is also why this sort of thing keeps working.

The FBI’s wider reporting on Business Email Compromise shows the scale of the problem. BEC has produced staggering losses over time, and the bureau’s own public advisory makes clear that this scam hits everyone from small local businesses to larger organisations. In other words, this is not an edge case. It is not rare. It is not exotic. It is a well worn criminal business model because human beings remain wonderfully efficient at trusting messages that seem to fit the moment.

Criminals do not always need advanced tooling.

Sometimes they just need your payable process and a decent lie.

This is not “just phishing”

Here is another trap.

People hear the word “phishing” and think of laughably bad emails from fake delivery firms, absurd grammar, and a logo pasted in by somebody half asleep. That still exists. It is also yesterday’s problem.

Modern social engineering can be tailored, patient, and unnervingly believable. The attacker may know the supplier name. They may know the project. They may know who approves invoices. They may mirror an email style, copy a signature block, and time the approach to fit a known payment cycle. They may compromise an account somewhere in the chain. Or they may simply spoof well enough to create confusion.

From the victim’s side, the effect is the same.

The request looks normal enough to get over the first hurdle.

And once it crosses that hurdle, a weak process does the rest.

So no, this is not “just phishing” in the lazy, checkbox training sense. This is social engineering aimed straight at money. It is phishing with a commercial objective. It is fraud dressed up as routine business.

Which raises a fair question.

How many of your internal controls were designed for exactly that?

The ugly truth about invoice fraud controls

A lot of businesses tell themselves they have controls because there is a policy document somewhere. That is lovely. Policies are nice. They can also be spectacularly useless when real life arrives wearing a supplier logo and asking for urgency.

What matters is not the document.

What matters is what your team actually does when an email asks for money to move.

Here is what sensible organisations put in place.

1. Out of band verification for bank detail changes

If somebody asks to change bank details, you verify that request using a known trusted route. Not the phone number in the email. Not the number in the signature. Not the friendly “call me on this direct line” added at the bottom.

You use a number already on file. A real contact. A route you trust.

This sounds obvious. It should be obvious. And yet this simple step is still absent in far too many businesses.

Why?

Because people confuse convenience with efficiency.

Convenience gets you robbed.

2. Dual authorisation for larger payments

No single person should be able to release a serious payment after a change request without a second human checking the details properly.

Not glancing.

Checking.

That second reviewer must know what they are looking for. “Yes, approved” is not a control if the approver has no context, no accountability, and no training.

And no, sending the approval request to another exhausted person ten minutes before close of play does not count as a robust process. That is just shared negligence with extra steps.

3. Supplier master data control

Who can edit supplier bank details in your finance system?

How is that logged?

Who reviews those changes?

How quickly can you see what changed, who changed it, and why?

If your answer is vague, you have a problem. A criminal only needs one weak doorway into your payment workflow. Change control around supplier records should be dull, controlled, and heavily logged. Boring is good here. Boring stops fraud.

4. Training that reflects real fraud, not theatre

Most security awareness training is about as useful as a chocolate fireguard.

There, I said it.

Too much of it is annual, generic, and forgettable. Staff click through it while thinking about lunch. Then leadership congratulates itself for “raising awareness” and moves on.

Real training uses real scenarios.

It teaches finance teams how invoice redirection works. It shows procurement and project staff what to look for. It explains why urgency, authority, and familiarity are classic social engineering levers. It drills the response. It repeats the lesson.

Because people do not rise to the level of policy. They fall to the level of habit.

5. Incident response for financial fraud, not just cyber incidents

If a fraudulent transfer happens, what do you do in the first 30 minutes?

Who calls the bank?

Who freezes approvals?

Who preserves emails and logs?

Who informs leadership?

Who contacts law enforcement?

Who owns vendor communication?

If your incident response plan only talks about malware, outages, and data breaches, you are missing a large and expensive category of modern cyber enabled fraud.

The bit that should really sting

The City of Arab says the scam was limited to one financial transaction. That is awful enough.

But imagine the same playbook hitting your business three times in a quarter.

One supplier payment.

One payroll diversion.

One fake “urgent transfer” supposedly from a director while they are travelling.

Could you absorb that?

Could your cash flow?

Could your reputation?

Could your staff confidence?

Could your customer relationships?

For a large organisation, invoice fraud hurts. For an SMB, it can be a body blow. Sometimes it is the thing that tips a strained business from “tough year” into “we are now having conversations with the bank that nobody enjoys”.

That is why I keep banging on about cyber as a business risk. Because it is. This is not just an IT department problem. Finance owns part of it. Operations owns part of it. Leadership owns all of it.

If the board, owner, or senior team still thinks cyber begins and ends with antivirus, they are staring at the wrong end of the problem.

Five questions you should ask your team today

Not next month. Not when you have “a bit more time”. Today.

1. How do we verify bank detail changes?

Can somebody explain the process clearly, or is it a fog of assumptions?

2. What payment threshold triggers dual approval?

And is that threshold sensible for the size of your business?

3. Who can amend supplier records?

Do you log changes, review them, and alert on them?

4. What fraud scenarios do we train on?

Is invoice fraud included, or are you still pretending every threat arrives as malware?

5. If a payment is sent in error, what happens in the first hour?

Do people know who calls the bank and what to say?

If those answers are weak, messy, or dependent on one person who “just knows how it works”, you do not have a process. You have folklore.

Folklore is charming in villages and terrible in finance.

What good looks like for a UK SMB

You do not need a ten million pound cyber budget to reduce this risk.

You do need discipline.

A sensible small business can improve massively by doing the following:

- enforce a hard rule that all supplier bank detail changes are verified by phone using known numbers

- require two people for high value payments and any payment linked to changed banking details

- lock down who can edit supplier records in the finance platform

- log and review those changes

- train finance, procurement, and leadership on real invoice fraud scenarios

- encourage staff to slow down when a payment request carries urgency

- make it culturally acceptable to challenge odd requests, even from senior people

- document what happens if a fraudulent transfer is discovered

Notice what is not on that list.

Expensive nonsense.

Most of this is process, culture, and basic control design. Technology supports it, yes. Email security helps. MFA helps. Domain protections help. Auditing helps. Logging helps. But none of that removes the need for proper financial controls.

If your cyber strategy never talks to your finance controls, you are building half a bridge and congratulating yourself for crossing the river.

“But our people know our suppliers”

Good. So did plenty of victims before the money left.

Trust is not useless. Business runs on trust. But trust without verification is how you end up funding a criminal’s next holiday.

Attackers rely on the fact that people know the supplier. That is the whole point. They do not want the request to feel alien. They want it to feel routine. They want familiarity to lower the guard.

That is why a known supplier can be more dangerous in this context than a random stranger.

The relationship becomes the attack surface.

What to do if you think you have been hit

Move quickly.

Really quickly.

Contact your bank immediately and ask for the transfer recall process. Preserve the email trail. Lock down any related approvals. Review supplier details. Inform your leadership team. Report it to law enforcement and your relevant cyber reporting channels. Do not let embarrassment slow you down.

Fraudsters love delay.

Every minute lost to internal panic, blame, or denial improves the odds that the money disappears through another hop and becomes much harder to recover.

And while you deal with the immediate crisis, do not let people hand wave it away as “just an accounting issue”. It is not. It is a cyber enabled fraud event with process, technology, human, and governance components.

Treat it with the seriousness it deserves.

The real lesson

The cautionary tale here is not that one city in Alabama got unlucky.

It is that this sort of fraud remains brutally effective because too many organisations still prepare for the wrong version of cyber risk. They picture drama. Criminals bring routine. They picture malware. Criminals send paperwork. They picture technical wizardry. Criminals exploit trust, timing, and weak approval processes.

One fake invoice.

One believable message.

One payment flow with a crack in it.

That is all it takes.

So what should you do with this story?

Do not just nod along and share it on LinkedIn with a solemn face and a few clapping emojis. Use it. Walk it straight into your next leadership meeting. Ask how your business would stop the same thing. Ask finance to explain the control path. Ask procurement how supplier detail changes are verified. Ask your IT provider what protections support the process. Ask who owns the response if the worst happens.

Then fix the weak bits before somebody else finds them for you.

Because if a payment can be redirected with nothing more glamorous than social engineering and a fake invoice, then your biggest cyber risk might not be sitting in the server room.

It might be sitting quietly in the inbox, waiting for somebody to press approve.

Sources

| Source | Link |

|---|---|

| City of Arab official press release, 6 March 2026 | arabcity.org |

| FBI press release, 2024 Internet Crime Report | fbi.gov |

| FBI IC3 advisory, Business Email Compromise: The $55 Billion Scam | ic3.gov |

| 256 Today coverage of the Arab incident | 256today.com |